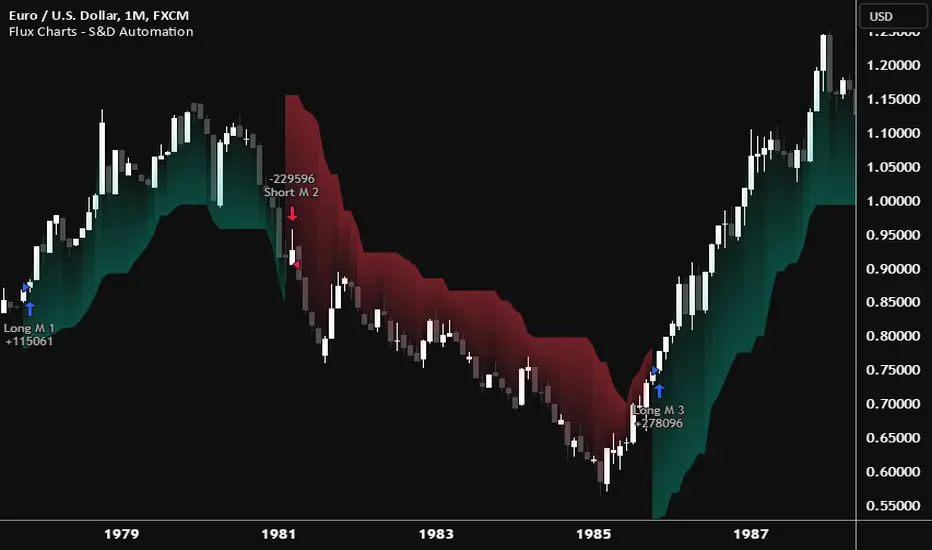

Flux Charts - S&D Automation💎 GENERAL OVERVIEW

The MTF Supply & Demand Zones (S&D) Automation is a powerful and versatile tool designed to help traders rigorously test their trading strategies against historical market data. With various advanced settings, traders can fine-tune their strategies, assess performance, and identify key improvements before deploying in live trading environments. This tool offers a wide range of configurable settings, explained within this write-up.

Features of the new S&D Automation:

Step By Step : Configure your strategy step by step, which will allow you to have OR & AND logic in your strategies.

Highly Configurable : Offers multiple parameters for fine-tuning trade entry and exit conditions.

Multi-Timeframe Analysis : Allows traders to analyze multiple timeframes simultaneously for enhanced accuracy.

Provides advanced stop-loss, take-profit, and break-even settings.

Incorporates Supply & Demand Zone conditions, with settings like Sensitivity, Zone Invalidation, Minimum Zone Width & Minimum Zone Length settings for refined strategy execution.

🚩 UNIQUENESS

The S&D Automation stands out from conventional backtesting tools due to its unparalleled flexibility, precision, and advanced trading logic integration. Key factors that make it unique include:

✅ Comprehensive Strategy Customization – Unlike traditional backtesters that offer basic entry and exit conditions, S&D Automation provides a highly detailed parameter set, allowing traders to fine-tune their strategies with precision.

✅ Multi-Timeframe Supply & Demand Zones – This is the first-ever tool that allows traders to backtest Supply & Demand zones on multiple timeframes.

✅ Customizable Take-Profit Conditions – Offers various methods to set take-profit exits, including using core features from Supply & Demand Zones, and fixed exits like ATR, % change or price change, enabling traders to tailor their exit strategies to specific market behaviors.

✅ Customizable Stop-Loss Conditions – Provides several ways to set up stop losses, including using concepts from Supply & Demand Zones and trailing stops or fixed exits like ATR, % change or price change, allowing for dynamic risk management tailored to individual strategies.

✅ Integration of External Indicators – Allows the inclusion of other indicators or data sources from TradingView for creating strategy conditions, enabling traders to enhance their strategies with additional insights and data points.

By integrating these advanced features, S&D Automation ensures that traders can rigorously test and optimize their strategies with great accuracy and efficiency.

📌 HOW DOES IT WORK ?

The first setting you will want to set it the pyramiding setting. This setting controls the number of simultaneous trades in the same direction allowed in the strategy. For example, if you set it to 1, only one trade can be active in any time, and the second trade will not be entered unless the first one is exited. If it is set to 2, the script will handle both of them at the same time. Note that you should enter the same value to this pyramiding setting, and the pyramiding setting in the "Properties" tab of the script for this to work.

You can enable and set a backtesting window that will limit the entries to between the start date & end date.

Then, you can enter your desired settings for Supply & Demand Zones. You can also enable and set up to 3 timeframes, which you can use later on when customizing your strategies enter / exit conditions.

Entry Conditions

From the "Long Conditions" or the "Short Conditions" groups, you can set your position entry conditions. For settings like "initial capital" or "order size", you can open the "Properties" tab, where these are handled.

The S&D Automation can use the following conditions for entry conditions :

1. Demand Zone

Detection: Triggered when a Demand Zone forms or is detected

Retest: Triggered when price retests a Demand Zone. A retest is confirmed when a candle enters a Demand Zone and closes outside of it.

2nd Retest: Triggered when price retests a Demand Zone for the second time. A retest is confirmed when a candle enters a Demand Zone and closes outside of it.

3rd Retest: Triggered when price retests a Demand Zone for the third time. A retest is confirmed when a candle enters a Demand Zone and closes outside of it.

Retracement: Triggered when price touches a Demand Zone

Break: Triggered when a Demand Zone is invalidated by candle close or wick, depending on the user's input.

2. Supply Zone

Detection: Triggered when a Supply Zone forms or is detected

Retest: Triggered when price retests a Supply Zone. A retest is confirmed when a candle enters a Supply Zone and closes outside of it.

2nd Retest: Triggered when price retests a Supply Zone for the second time. A retest is confirmed when a candle enters a Supply Zone and closes outside of it.

3rd Retest: Triggered when price retests a Supply Zone for the third time. A retest is confirmed when a candle enters a Supply Zone and closes outside of it.

Retracement: Triggered when price touches a Supply Zone

Break: Triggered when a Supply Zone is invalidated by candle close or wick, depending on the user's input.

3. Any Zone

Detection: Triggered when any Supply or Demand Zone forms or is detected

Retest: Triggered when price retests any Supply or Demand Zone. A retest is confirmed when a candle enters any Supply or Demand Zone and closes outside of it.

2nd Retest: Triggered when price retests any Supply or Demand Zone for the second time. A retest is confirmed when a candle enters any Supply or Demand Zone and closes outside of it.

3rd Retest: Triggered when price retests any Supply or Demand Zone for the third time. A retest is confirmed when a candle enters any Supply or Demand Zone and closes outside of it.

Retracement: Triggered when price touches any Supply or Demand Zone

Break: Triggered when any Supply or Demand Zone is invalidated by candle close or wick, depending on the user's input.

🕒 TIMEFRAME CONDITIONS

The S&D Automation supports Multi-Timeframe (MTF) features, just like the Supply & Demand indicator. When setting an entry condition, you can also choose the timeframe.

To set up MTF conditions, navigate to the 'Timeframes' section in the settings, select your desired timeframes, and enable them. You can choose up to three timeframes.

Once you've selected your timeframes, you can use them in your strategy. When setting long and short entry/exit conditions, you can choose from Timeframe 1, Timeframe 2, or Timeframe 3.

External Conditions

Users can use external indicators on the chart to set entry conditions.

The second dropdown in the external condition settings allows you to choose a conditional operator to compare external outputs. Available options include:

Less Than or Equal To: <=

Less Than: <

Equal To: =

Greater Than: >

Greater Than or Equal To: >=

The position entry conditions work like this ;

Each side has 5 S&D Zone conditions and 1 Source condition. Each condition can be enabled or disabled using the checkbox on the left side of them.

The next selection is the alert type, which you can select between "Detection", "Retest", "Retracement" or "Break".

You can select which timeframe this condition should work on from Timeframe 1, 2, or 3. If you select "Any Timeframe", the condition will work for all timeframes.

Lastly select the step of this condition from 1 to 6.

The Source Condition

The last condition on each side is a source condition that is different from the others. Using this condition, you can create your own logic using other indicators' outputs on your chart. For example, suppose that you have an EMA indicator in your chart. You can have the source condition to something like "EMA > high".

The Step System

Each condition has a step number, and conditions are in topological order based on them.

The conditions are executed step by step. This means the condition with step 2 cannot be executed before the condition with step 1 is executed.

Conditions with the same step numbers have "OR" logic. This means that if you have 2 conditions with step 3, the condition with step 4 can trigger after only one of the step 3 conditions is executed.

➕ OTHER ENTRY FEATURES

The S&D Automation allows traders to choose when to execute trades and when not to execute trades.

1. Only Take Trades

This setting lets users specify the time period when their strategy can open or execute trades.

2. Don't Take Trades

This setting lets users specify time periods when their strategy can't open or execute trades.

↩️ EXIT CONDITIONS

1. Exit on Opposite Signal

When enabled, a long position will close when short entry conditions are met, and a short position will close when long entry conditions are met.

2. Exit on Session End

When enabled, positions will be closed at the end of the trading session.

📈 TAKE PROFIT CONDITIONS

There are several methods available for setting take profit exits and conditions.

1. Entry Condition TP

Users can use entry conditions as triggers for take-profit exits. This setting can be found under the long and short exit conditions.

2. Fixed TP

Users can set a fixed TP for exits. This setting can be found under the long and short exit conditions. Users can choose between the following:

Price: This method triggers a TP exit when price reaches a specified level. For example, if you set the Price TP to 10 and buy NASDAQ:TSLA at $190, the trade will automatically exit when the price reaches $200 ($190 + $10).

Ticks: This method triggers a TP exit when price moves a specified number of ticks.

Percentage (%): This method triggers a TP exit when price moves a specified percentage.

ATR: This method triggers a TP exit based on a specified multiple of the Average True Range (ATR).

📉 STOP LOSS CONDITIONS

There are several methods available for setting stop-loss exits and conditions.

1. Entry Condition SL

Users can use entry conditions as triggers for stop-loss exits. This setting can be found under the long and short exit conditions.

2. Fixed SL

Users can set a fixed SL for exits. This setting can be found under the long and short exit conditions. Users can choose between the following:

Price: This method triggers a SL exit when price reaches a specified level. For example, if you set the Price SL to 10 and buy NASDAQ:TSLA at $200, the trade will automatically exit when the price reaches $190 ($200 - $10).

Ticks: This method triggers a SL exit when price moves a specified number of ticks.

Percentage (%): This method triggers a SL exit when price moves a specified percentage.

ATR: This method triggers a SL exit based on a specified multiple of the Average True Range (ATR).

3. Trailing Stop

An explanation & example for the trailing stop feature is present on the write-up within the next section.

Exit conditions have the same logic of constructing conditions like the entry ones. You can construct a Take-Profit Condition & a Stop-Loss Condition. Note that the Take-Profit condition will only work if the position is in profit, regardless of if it's triggered or not. The same applies for the Stop-Loss condition, meaning that it will only work if the position is in loss.

You can also set a Fixed TP & Fixed SL based on the price movement after the position is entered. You have options like "Price", "Ticks", "%", or "Average True Range". For example, you can set a Fixed TP like "5%", and the position will be entered once it moves 5% up in a long position.

Trailing Stop

For the Fixed SL, you also have a "Trailing" stop option, for which you can set its activation level as well. The Trailing stop activation level and its value are expressed in ticks. Check this scenario for an example :

We have a ticker with a tick value of $1. Our Trailing Stop is set to 10 ticks, and the activation level is set to 30 ticks.

We buy 1 contract when the price is $100.

When the price becomes $110, we are in $10 (10 ticks) profit and the trailing stop is now activated.

The current price our stop's on is $110 - $30 (30 ticks), which is the level of $80.

The trailing stop will only move if the price moves up the highest high the price has been after we entered the position.

Let's suppose that price moves up $40 right after our trailing stop is activated. The price will now be $150, and our trailing stop will sit on $150 - $30 (30 ticks) = $120.

If the price is down the $120 level, our stop loss will be triggered.

There is also a "Hard SL" option designed for a backup stop-loss when trailing stops are enabled. You can enable & set this option and if the price goes down before our trailing stop even activates, the position will be exited.

You can also move stop-loss to the break-even (entry price of the position) after a certain profit is achieved using the last setting of the exit conditions. Note that for this to work, you must have a Fixed SL set-up.

➕ OTHER EXIT FEATURES

1. Move Stop Loss to Breakeven

This setting allows the strategy to automatically move the SL to Breakeven (BE) when the position is in profit by a certain amount. Users can choose between the following:

Price: This method moves the SL to BE when price reaches a specified level.

Ticks: This method moves the SL to BE when price moves a specified number of ticks.

Percentage (%): This method moves the SL to BE when price moves a specified percentage.

ATR: This method moves the SL to BE when price moves a specified multiple of the Average True Range (ATR).

Example Entry Scenario

To give an example , check this scenario; out conditions are :

LONG CONDITIONS

Demand Zone Detection, Step 1

Supply Zone Retest, Step 2

Demand Zone Break, Step 2

open > close, Step 3

First, the strategy needs to detect a Demand Zone Detection in order to start working.

After it's detected, now it's looking for either a Supply Zone Retest, or a Demand Zone Break to proceed to the next step, the reason for this is that they both have the same step number.

After one of them is detected, the strategy will consistently check candlesticks for the condition open > close. If a bullish candlestick occurs, a long position will be entered.

⏰ ALERTS

This indicator uses TradingView's strategy alert system. All entries and exits will be sent as an alert if configured. It's possible to further customize these alerts to your liking. For more information check TradingView's strategy alert customization page : www.tradingview.com

⚙️ SETTINGS

1. Backtesting Settings

Pyramiding: Controls the number of simultaneous trades allowed in the strategy. This setting must have the same value that is entered on the script's properties tab on the settings pane.

Enable Custom Backtesting Period: Restricts backtesting to a specific date range.

Start & End Time Configuration: Define precise start and end dates for historical analysis.

2. General Configuration

Detection Method: There are two detection methods you can choose from for identifying Supply & Demand Zones. Both methods aim to identify key areas where price is likely to react, but they do so using different approaches. Traders can choose the method that aligns with their trading style and time horizon.

Sensitivity: The Sensitivity setting allows traders to adjust how aggressively the script identifies supply and demand zones when using the Momentum Detection Method. This setting directly impacts the threshold for detecting zones when using the momentum detection method.

Zone Invalidation: The Zone Invalidation setting determines how supply and demand zones are invalidated.

Wick -> A zone is invalidated if a candle’s wick goes below a demand zone or above a supply zone.

Close -> A zone is invalidated if a candle closes below a demand zone or above a supply zone.

Zone Visibility Range: The Zone Visibility Range setting controls how far from the current price supply and demand zones are displayed on the chart. It helps traders focus on relevant zones while avoiding clutter from distant or less impactful areas.

Minimum Zone Width: The Minimum Zone Width setting defines the smallest size a supply or demand zone must have to be displayed on the chart. It uses the Average True Range (ATR) as a reference to ensure zones are proportionate to current market volatility.

Minimum Zone Length: The Minimum Zone Length setting determines the minimum number of bars a supply or demand zone must span to be displayed on the chart. This setting helps filter out short-lived or insignificant zones, ensuring only meaningful areas of supply or demand are highlighted.

3. Multi-Timeframe Analysis

Enable Up to Three Timeframes: Select and analyze trades across multiple timeframes.

4. Entry Conditions for Long & Short Trades

Multiple Conditions (1-6): Configure up to six independent conditions per trade direction.

Condition Types: Options include Detection, Retest, 2nd Retest, 3rd Retest, Retracement, and Break.

Timeframe Specification: Choose between "Any Timeframe", "Timeframe 1", "Timeframe 2", or "Timeframe 3".

Trade Execution Filters: Restrict trades within specific trading sessions.

5. Exit Conditions for Long & Short Trades

Exit on Opposite Signal: Automatically exit trades upon opposite trade conditions.

Exit on Session End: Closes all positions at the end of the trading session.

Multiple Take-Profit (TP) and Stop-Loss (SL) Configurations:

TP/SL based on % move, ATR, Ticks, or Fixed Price.

Hard SL option for additional risk control.

Move SL to BE (Break Even) after a certain profit threshold.

Cerca negli script per "stop loss"

Flux Charts - PAT Automation💎 GENERAL OVERVIEW

The PAT Automation is a powerful and versatile tool designed to help traders rigorously test their trading strategies against historical market data. With an array of advanced settings, traders can fine-tune their strategies, assess performance, and identify key improvements before deploying in live trading environments. This backtester offers a wide range of configurable settings, explained within this write-up.

Features of the PAT Automation:

Step By Step : Configure your strategy step by step, which will allow you to have OR & AND logic in your strategies.

Highly Configurable : Offers multiple parameters for fine-tuning trade entry and exit conditions.

Multi-Timeframe Analysis : Allows traders to analyze multiple timeframes simultaneously for enhanced accuracy.

Provides advanced stop-loss, take-profit, and break-even settings.

Incorporates volume-based conditions, liquidity grabs , order blocks , market structures and fair value gaps for refined strategy execution.

🚩 UNIQUENESS

The PAT Automation stands out from conventional backtesting tools due to its unparalleled flexibility, precision, and advanced trading logic integration. Key factors that make it unique include:

✅ Comprehensive Strategy Customization – Unlike traditional backtesters that offer basic entry and exit conditions, PAT Automation provides a highly detailed parameter set, allowing traders to fine-tune their strategies with precision.

✅ Multi-Timeframe Price Action Features – This is the first-ever tool that allows traders to backtest price action with multi-timeframe features such as Fair Value Gaps (FVGs), Inversion Fair Value Gaps (IFVGs), Order Blocks & Breaker Blocks.

✅ Customizable Take-Profit Conditions – Offers various methods to set take-profit exits, including using core features from price action, and fixed exits like ATR, % change or price change, enabling traders to tailor their exit strategies to specific market behaviors.

✅ Customizable Stop-Loss Conditions – Provides several ways to set up stop losses, including using concepts from price action and trailing stops or fixed exits like ATR, % change or price change, allowing for dynamic risk management tailored to individual strategies.

✅ Integration of External Indicators – Allows the inclusion of other indicators or data sources from TradingView for creating strategy conditions, enabling traders to enhance their strategies with additional insights and data points.

By integrating these advanced features, PAT Automation ensures that traders can rigorously test and optimize their strategies with great accuracy and efficiency.

📌 HOW DOES IT WORK?

The first setting you will want to set it the pyramiding setting. This setting controls the number of simultaneous trades in the same direction allowed in the strategy. For example, if you set it to 1, only one trade can be active in any time, and the second trade will not be entered unless the first one is exited. If it is set to 2, the script will handle both of them at the same time. Note that you should enter the same value to this pyramiding setting, and the pyramiding setting in the "Properties" tab of the script for this to work.

For deep backtesting, you can set "Max Distance To Last Bar" to "Unlimited". If you encounter any memory issues, try decreasing this setting to a lower value.

You can enable and set a backtesting window that will limit the entries to between the start date & end date.

Then, you can enter your desired settings to Price Action features like FVGs, IFVGs, Order Blocks, Breaker Blocks, Liquidity Grabs, Market Structures, EQH & EQL and Volume Imbalances. You can also enable and set up to 3 timeframes, which you can use later on when customizing your strategies enter / exit conditions.

Entry Conditions

From the "Long Conditions" or the "Short Conditions" groups, you can set your position entry conditions. For settings like "initial capital" or "order size", you can open the "Properties" tab, where these are handled.

The PAT Automation can use the following conditions for entry conditions :

1. Order Block (OB)

Detection: Triggered when an Order Block forms or is detected

Retest: Triggered when price retests an Order Block. A retest is confirmed when a candle enters an Order Block and closes outside of it.

Retracement: Triggered when price touches an Order Block

Break: Triggered when an Order Block is invalidated by candle close or wick, depending on the user's input.

2. Breaker Block (BB)

Detection: Triggered when a Breaker Block forms or is detected

Retest: Triggered when price retests a Breaker Block. A retest is confirmed when a candle enters a Breaker Block and closes outside of it.

Retracement: Triggered when price touches a Breaker Block

Break: Triggered when a Breaker Block is invalidated by candle close or wick, depending on the user's input.

3. Fair Value Gap (FVG)

Detection: Triggered when an FVG forms or is detected

Retest: Triggered when price retests an FVG. A retest is confirmed when a candle enters an FVG and closes outside of it.

Retracement: Triggered when price touches an FVG

Break: Triggered when an FVG is invalidated by candle close or wick, depending on the user's input.

4. Inversion Fair Value Gap (IFVG)

Detection: Triggered when an IFVG forms or is detected

Retest: Triggered when price retests an IFVG. A retest is confirmed when a candle enters an IFVG and closes outside of it.

Retracement: Triggered when price touches an IFVG

Break: Triggered when an IFVG is invalidated by candle close or wick, depending on the user's input.

5. Break of Structure (BOS)

Detection: Triggered when a BOS forms or is detected

6. Change of Character (CHoCH)

Detection: Triggered when a CHoCH forms or is detected

7. Change of Character Plus (CHoCH+)

Detection: Triggered when a CHoCH+ forms or is detected

8. Volume Imbalance (VI)

Detection: Triggered when a Volume Imbalance forms or is detected

9. Equal High (EQH)

Detection: Triggered when an EQH is detected

10. Equal Low (EQL)

Detection: Triggered when an EQL is detected

11. Buyside Liquidity Grab

Detection: Triggered when a liquidity grab occurs at Buyside Liquidity (BSL).

12. Sellside Liquidity Grab

Detection: Triggered when a liquidity grab occurs at Sellside Liquidity (SSL).

🕒 TIMEFRAME CONDITIONS

The PAT Automation supports Multi-Timeframe (MTF) features, just like the Price Action Toolkit. When setting an entry condition, you can also choose the timeframe.

To set up MTF conditions, navigate to the 'Timeframes' section in the settings, select your desired timeframes, and enable them. You can choose up to three timeframes.

Once you've selected your timeframes, you can use them in your strategy. When setting long and short entry / exit conditions, you can choose from Timeframe 1, Timeframe 2, or Timeframe 3.

External Conditions

Users can use external indicators on the chart to set entry conditions.

The second dropdown in the external condition settings allows you to choose a conditional operator to compare external outputs. Available options include:

Less Than or Equal To: <=

Less Than: <

Equal To: =

Greater Than: >

Greater Than or Equal To: >=

The position entry conditions work like this ;

Each side has 5 Price Action conditions and 1 Source condition. Each condition can be enabled or disabled using the checkbox on the left side.

For Price Action Conditions, you can set a direction: "Any", "Bullish" or "Bearish".

Then a Price Action Feature, like "FVG" or "Order Block".

The last part of our constructed condition is the alert type, which you can select between "Detection", "Retest", "Retracement" or "Break".

Now you should have a constructed condition, which should look like "Bullish Order Block Retest".

You can select which timeframe should this condition work on from Timeframe 1, 2 or 3. If you select "Any Timeframe", the condition will work for all timeframes.

Lastly select the step of this condition from 1 to 6.

The Source Condition

The last condition on each side is a source condition that is different from the others. Using this condition, you can create your own logic using other indicators' outputs on your chart. For example, suppose that you have an EMA indicator in your chart. You can have the source condition to something like "EMA > high".

The Step System

Each condition has a step number, and conditions are in topological order based on them.

The conditions are executed step by step. This means the condition with step 2 cannot be executed before the condition with step 1 is executed.

Conditions with the same step numbers have "OR" logic. This means that if you have 2 conditions with step 3, the condition with step 4 can trigger after only one of the step 3 conditions is executed.

➕ OTHER ENTRY FEATURES

The PAT Automation allows traders to choose when to execute trades and when not to execute trades.

1. Only Take Trades

This setting lets users specify the time period when their strategy can open or execute trades.

2. Don't Take Trades

This setting lets users specify time periods when their strategy can't open or execute trades.

↩️ EXIT CONDITIONS

1. Exit on Opposite Signal

When enabled, a long position will close when short entry conditions are met, and a short position will close when long entry conditions are met.

2. Exit on Session End

When enabled, positions will be closed at the end of the trading session.

📈 TAKE PROFIT CONDITIONS

There are several methods available for setting take profit exits and conditions.

1. Entry Condition TP

Users can use entry conditions as triggers for take-profit exits. This setting can be found under the long and short exit conditions.

2. Fixed TP

Users can set a fixed TP for exits. This setting can be found under the long and short exit conditions. Users can choose between the following:

Price: This method triggers a TP exit when price reaches a specified level. For example, if you set the Price TP to 10 and buy NASDAQ:TSLA at $190, the trade will automatically exit when the price reaches $200 ($190 + $10).

Ticks: This method triggers a TP exit when price moves a specified number of ticks.

Percentage (%): This method triggers a TP exit when price moves a specified percentage.

ATR: This method triggers a TP exit based on a specified multiple of the Average True Range (ATR).

📉 STOP LOSS CONDITIONS

There are several methods available for setting stop-loss exits and conditions.

1. Entry Condition SL

Users can use entry conditions as triggers for stop-loss exits. This setting can be found under the long and short exit conditions.

2. Fixed SL

Users can set a fixed SL for exits. This setting can be found under the long and short exit conditions. Users can choose between the following:

Price: This method triggers a SL exit when price reaches a specified level. For example, if you set the Price SL to 10 and buy NASDAQ:TSLA at $200, the trade will automatically exit when the price reaches $190 ($200 - $10).

Ticks: This method triggers a SL exit when price moves a specified number of ticks.

Percentage (%): This method triggers a SL exit when price moves a specified percentage.

ATR: This method triggers a SL exit based on a specified multiple of the Average True Range (ATR).

3. Trailing Stop

An explanation & example for the trailing stop feature is present on the write-up within the next section.

Exit conditions have the same logic of constructing conditions like the entry ones. You can construct a Take-Profit Condition & a Stop-Loss Condition. Note that the Take-Profit condition will only work if the position is in profit, regardless of if it's triggered or not. The same applies for the Stop-Loss condition, meaning that it will only work if the position is in loss.

You can also set a Fixed TP & Fixed SL based on the price movement after the position is entered. You have options like "Price", "Ticks", "%", or "Average True Range". For example, you can set a Fixed TP like "5%", and the position will be entered once it moves 5% up in a long position.

Trailing Stop

For the Fixed SL, you also have a "Trailing" stop option, which you can set it's activation level as well. The Trailing stop activation level and it's value are expressed in ticks. Check this scenerio for an example :

We have a ticker with a tick value of $1. Our Trailing Stop is set to 10 ticks and activation level is set to 30 ticks.

We buy 1 contract when the price is $100.

When the price becomes $110, we are in $10 (10 ticks) profit and the trailing stop is now activated.

The current price our stop's on is $110 - $30 (30 ticks), which is the level of $80.

The trailing stop will only move if the price moves up the highest high the price has been after we entered the position.

Let's suppose that price moves up $40 right after our trailing stop is activated. The price will now be $150, and our trailing stop will sit on $150 - $30 (30 ticks) = $120.

If the price is down the $120 level, our stop loss will be triggered.

There is also a "Hard SL" option designed for a backup stop-loss when trailing stops are enabled. You can enable & set this option and if the price goes down before our trailing stop even activates, the position will be exited.

You can also move stop-loss to the break-even (entry price of the position) after a certain profit is achieved using the last setting of the exit conditions. Note that for this to work, you will need to have a Fixed SL set-up.

➕ OTHER EXIT FEATURES

1. Move Stop Loss to Breakeven

This setting allows the strategy to automatically move the SL to Breakeven (BE) when the position is in profit by a certain amount. Users can choose between the following:

Price: This method moves the SL to BE when price reaches a specified level.

Ticks: This method moves the SL to BE when price moves a specified number of ticks.

Percentage (%): This method moves the SL to BE when price moves a specified percentage.

ATR: This method moves the SL to BE when price moves a specified multiple of the Average True Range (ATR).

Example Entry Scenario

To give an example , check this scenario; out conditions are :

LONG CONDITIONS

Bullish Order Block Detection, Step 1

Bullish CHoCH Detection, Step 2

Bullish Volume Imbalance Detection, Step 2

Bullish IFVG Retest, Step 3

First, the strategy needs to detect a Bullish Order Block in order to start working.

After it's detected, now it's looking for either a CHoCH, or a Volume Imbalance to proceed to the next step, the reason for this is that they both have the same step number.

After one of them is detected, the strategy will consistently check all IFVGs for a retest. If the retest occurs, a long position will be entered.

⏰ ALERTS

This indicator uses TradingView's strategy alert system. All entries and exits will be sent as an alert if configured. It's possible to further customize these alerts to your liking. For more information check TradingView's strategy alert customization page: www.tradingview.com

⚙️ SETTINGS

1. Backtesting Settings

Pyramiding: Controls the number of simultaneous trades allowed in the strategy. This setting must have the same value that is entered on the script's properties tab on the settings pane.

Max Distance to Last Bar: Determines the depth of historical data used to prevent memory overload.

Enable Custom Backtesting Period: Restricts backtesting to a specific date range.

Start & End Time Configuration: Define precise start and end dates for historical analysis.

2. Fair Value Gaps Settings

Zone Invalidation: Select between "Wick" and "Close" invalidation.

Filtering: Choose between "Average Range" and "Volume Threshold".

FVG Sensitivity: Ranges from Extreme to Low to detect FVGs with varying strictness.

Allow Gaps: Enables analysis on tickers that have different open-close price gaps.

3. Inversion Fair Value Gaps Settings

Zone Invalidation: Choose between "Wick" and "Close".

4. Order Block Settings

Swing Length: Adjusts the minimum number of bars required for OB formation.

Zone Invalidation Method: Select between "Wick" and "Close".

5. Breaker Block Settings

Zone Invalidation: Set invalidation method as "Wick" or "Close".

6. Liquidity Grabs Settings

Pivot Length: Adjusts the number of bars used to detect liquidity grabs.

Wick-Body Ratio: Defines the proportion of wick-to-body size for liquidity grab detection.

7. Multi-Timeframe Analysis

Enable Up to Three Timeframes: Select and analyze trades across multiple timeframes.

8. Market Structures

Swing Length: Defines the number of bars required for structure shifts.

Includes BOS, CHoCH, CHoCH+ Detection.

9. Equal Highs & Lows

ATR Multiplier: Defines the sensitivity of equal highs/lows detection.

10. Volume Imbalances

Gap Size Sensitivity: Ranges from "Ultra" to "Low".

Disable Overnight Gaps: Filters out volume imbalances occurring due to overnight gaps.

11. Entry Conditions for Long & Short Trades

Multiple Conditions (1-6): Configure up to six independent conditions per trade direction.

Condition Types: Options include Detection, Retest, Retracement, and Break.

Timeframe Specification: Choose between "Any Timeframe", "Timeframe 1", "Timeframe 2", or "Timeframe 3".

Trade Execution Filters: Restrict trades within specific trading sessions.

12. Exit Conditions for Long & Short Trades

Exit on Opposite Signal: Automatically exit trades upon opposite trade conditions.

Exit on Session End: Closes all positions at the end of the trading session.

Multiple Take-Profit (TP) and Stop-Loss (SL) Configurations:

TP/SL based on % move, ATR, Ticks, or Fixed Price.

Hard SL option for additional risk control.

Move SL to BE (Break Even) after a certain profit threshold.

Triple EMA Crossover StrategyTriple EMA Crossover Strategy

Overview

The Triple EMA Crossover Strategy is a trend-following trading system that utilizes three Exponential Moving Averages (EMAs) to identify potential entry and exit points in the market. This strategy is based on the principle that when shorter-term prices cross above longer-term prices, it can indicate a bullish trend, and conversely when they cross below, it can signal a bearish trend.

Components

Exponential Moving Averages (EMAs):

Short EMA: A fast-moving average that reacts quickly to price changes (commonly set to 9 periods).

Medium EMA: A medium-term average that smooths out price data and helps confirm trends (commonly set to 21 periods).

Long EMA: A slow-moving average that helps identify the overall trend direction (commonly set to 55 periods).

Trading Signals:

Buy Signal: A long entry is triggered when:

The Short EMA (9) crosses above the Medium EMA (21).

The Medium EMA (21) is above the Long EMA (55).

Sell Signal: A short entry is signaled when:

The Short EMA (9) crosses below the Medium EMA (21).

The Medium EMA (21) is below the Long EMA (55).

Stop Loss and Take Profit:

Stop Loss: Implement a predefined percentage or ATR-based stop loss to limit potential losses.

Take Profit: Set a target based on a risk-to-reward ratio that reflects your trading strategy's goals.

Advantages

Trend Identification: The EMA crossover system allows traders to identify the current trend dynamically, focusing on upward or downward price movements.

Simplicity: The strategy is straightforward, making it accessible for both new and experienced traders.

Flexibility: This method can be applied across multiple timeframes and asset classes, making it versatile for various trading styles.

Disadvantages

Lagging Indicator: Moving averages are lagging indicators, meaning signals may come later than the actual price movement, which can lead to missed opportunities.

Whipsaw Effect: In ranging markets, the strategy may produce false signals leading to potential losses.

ETH Signal 15m

This strategy uses the Supertrend indicator combined with RSI to generate buy and sell signals, with stop loss (SL) and take profit (TP) conditions based on ATR (Average True Range). Below is a detailed explanation of each part:

1. General Information BINANCE:ETHUSDT.P

Strategy Name: "ETH Signal 15m"

Designed for use on the 15-minute time frame for the ETH pair.

Default capital allocation is 15% of total equity for each trade.

2. Backtest Period

start_time and end_time: Define the start and end time of the backtest period.

start_time = 2024-08-01: Start date of the backtest.

end_time = 2054-01-01: End date of the backtest.

The strategy will only run when the current time falls within this specified range.

3. Supertrend Indicator

Supertrend is a trend-following indicator that provides buy or sell signals based on the direction of price changes.

factor = 2.76: The multiplier used in the Supertrend calculation (increasing this value makes the Supertrend less sensitive to price movements).

atrPeriod = 12: Number of periods used to calculate ATR.

Output:

direction: Determines the buy/sell direction based on Supertrend.

If direction decreases, it signals a buy (Long).

If direction increases, it signals a sell (Short).

4. RSI Indicator

RSI (Relative Strength Index) is a momentum indicator, often used to identify overbought or oversold conditions.

rsiLength = 12: Number of periods used to calculate RSI.

rsiOverbought = 70: RSI level considered overbought.

rsiOversold = 30: RSI level considered oversold.

5. Entry Conditions

Long Entry:

Supertrend gives a buy signal (ta.change(direction) < 0).

RSI must be below the overbought level (rsi < rsiOverbought).

Short Entry:

Supertrend gives a sell signal (ta.change(direction) > 0).

RSI must be above the oversold level (rsi > rsiOversold).

The strategy will only execute trades if the current time is within the backtest period (in_date_range).

6. Stop Loss (SL) and Take Profit (TP) Conditions

ATR (Average True Range) is used to calculate the distance for Stop Loss and Take Profit based on price volatility.

atr = ta.atr(atrPeriod): ATR is calculated using 12 periods.

Stop Loss and Take Profit are calculated as follows:

Long Trade:

Stop Loss: Set at close - 4 * atr (current price minus 4 times the ATR).

Take Profit: Set at close + 2 * atr (current price plus 2 times the ATR).

Short Trade:

Stop Loss: Set at close + 4 * atr (current price plus 4 times the ATR).

Take Profit: Set at close - 2.237 * atr (current price minus 2.237 times the ATR).

Summary:

This strategy enters a Long trade when the Supertrend indicates an upward trend and RSI is not in the overbought region. Conversely, a Short trade is entered when Supertrend signals a downtrend, and RSI is not oversold.

The trade is exited when the price reaches the Stop Loss or Take Profit levels, which are determined based on price volatility (ATR).

Disclaimer:

The content provided in this strategy is for informational and educational purposes only. It is not intended as financial, investment, or trading advice. Trading in cryptocurrency, stocks, or any financial markets involves significant risk, and you may lose more than your initial investment. Past performance is not indicative of future results, and no guarantee of profit can be made. You should consult with a professional financial advisor before making any investment decisions. The creator of this strategy is not responsible for any financial losses or damages incurred as a result of following this strategy. All trades are executed at your own risk.

Pullback_Power [JackTz]Welcome to Pullback_Power

Pullback_Power is a scalping strategy designed to capitalize on market retracements while incorporating unique dynamic features to enhance profitability.

Calculation

Pullback_Power purely uses moving averages to calculate both entry and exits. Exits can also be set to fixed percentages for both take profit and stop loss.

How the Strategy Works

Statistics show that markets normally do a recovery after each drop. Crypto markets can easily drop up to 20% within a few hours and then do a complete or partial recovery. Pullback_Power utilizes this known pattern alongside pyramiding. The strategy aims to catch one or more entries when the price drops, hoping to make profits when the market recovers from the drop. The fixed take profit and stop loss can be used to define your risk management, while the dynamic exit opportunity is riskier but provides the ability to stay in the trade longer while it recovers. Pullback_Power can make up to four entries. This means it utilizes pyramiding to spread out the entry points, but every exit is a full exit. It is not possible to partially exit.

Utility

Pullback_Power is a scalping strategy suitable for traders who operate with small trades and don't want to stay in the market for too long. Pullback_Power offers precise signals with no repainting. The strategy thrives in volatility, so crypto pairs might yield the best results, although this strategy can be adapted to work on all pairs and markets.

How to Automate It

Pullback_Power utilizes the standard placeholders of strategies on TradingView. This enables the trader to add every data point into a webhook, making it fully flexible to suit every trader's needs. To automate, create an alert, set the webhook URL, and add the JSON body needed for the webhook. An example of a simple JSON webhook with some of the standard strategy placeholders:

{

"side": "{{strategy.order.action}}",

"symbol": "{{ticker}}",

"amount": "{{strategy.order.contracts}}"

}

Read about all the standard placeholders that you can use here: TradingView - Standard strategy placeholders

Originality

Pullback_Power is unique in its ability to create precise signals without repainting while maintaining a solid approach to the pullback strategy. Its simplicity not only makes the strategy easy to use and understand but also highly effective. The simplicity reduces inputs, eliminating overfitting and limits each input to avoid incorrect usage. Many times, default settings are enough to achieve good backtesting results on almost all pairs available. Pullback_Power also differs from many other strategies by its solid code, which enhances performance and provides more reliable backtesting. The clean code increases the resilience and precision of the entries, making it less prone to errors.

Many pullback/scalping strategies normally only works on specific scopes of timeframes or pairs. Pullback_Power can easily be adapted to work on almost every scenario. The biggest change needed is the length of the moving average. The lower the timeframe, the higher a length is needed for proper results. I.e. on a 2H timeframe a length of 3 can yield good results. On a 5min timeframe the length might need to be as high as 70.

How to Use

To use Pullback_Power, add the script to your trading chart. By default, Pullback_Power opens four orders to optimize trade opportunities with a default fee value set at 0.1%. You can change these default settings in the Settings window under the Properties tab. To tailor Pullback_Power to your individual trading style, navigate to the Settings under the Input tab. Here you can configure various inputs to fit your trading style.

- Backtest settings , Start Date:

Defines the date of when the calculation starts. Use this to set the date of when the first trade could potentially emit.

- Backtest settings , End Date:

Defines the date of when the calculation ends. If there are any open trades after this date the close calculations are still live. It only makes sure that new orders cannot be opened after this date.

- Backtest settings , Only trade on weekdays:

This is a toggle you can enable or disable. If enabled it only allows new entries to happen during the normal week days, meaning Monday, Tuesday, Wednesday, Thursday and Friday.

Disable this to enable the script to open trades on all 7 days of the week.

- Open settings , Use dynamic long positions:

This toggle allows you to enable or disable the pullback level calculations after first trade.

If enabled, the calculations of level 2, 3 and 4 continues to happen after each bar, making the levels follow the price with the moving averages calculations.

If disabled, the calculations of the levels stop after the first trade. This means that the levels calculation at the point of the first trade stay fixed until all trades are closed.

You can see the difference of the green lines on the chart when you toggle this flag.

- Open settings , Data type:

This is the bar data used for the moving average calculation when opening trades. The possible data types are Open, High, Low, Close, HL2, HLC3, OHLC4, OC2 and HC2.

- Open settings , Source type:

This is the source used to calculate the moving average. The types available are: SMA, PCMA, EMA, WMA, DEMA, ZLEMA and HMA.

- Open settings , Length:

This is the length used for the moving average calculations. 3 means it takes the last 3 bars of historical data for the calculation.

- Open settings , Offset:

This defines if the calculation should use an offset for the historical data. This does not use a look-forward feature, but a look-backward feature. To prevent any possible repaints the offset can only be positive, not negative.

For instance, if the length is 3 and the offset is 0 the calculation is made from the last 3 bars, making it bar1, bar2 and bar3. If the length is 3 and the offset is 1 the calculation is made from bar2, bar3, and bar4 – offsetting the calculation by 1 bar.

- Leverage settings , Leverage liquidation (1-125):

The script itself does not handle any custom leverage calculation – this must be done in the Properties tabs and increasing the order size.

This setting is made to test a possible liquidation event if using leverage.

By setting this to higher than 1, a red line is visible after the first trade on the chart. This indicates the liquidation price.

If this setting is set to 25, the script will calculate the liquidation price from a x25 leverage. If this price is hit, the scripts stops emitting any orders and the background turns red.

You can use this to test if your settings could handle a certain level of leverage.

- Pullback settings , Pullback 1, 2, 3 and 4:

Each of these settings defines the entry price of each pullback level. If Pullback 1 is set to -6 it means that the moving average calculation should be 6% lower than the actual price.

The same logic applies to Pullback 2, 3 and 4.

Setting any level to 0 will disable the level – eliminating any orders to emit on that level.

This can be used to change the level of pyramiding down from 4 if needed.

If you do this, remember to also change the order size and the pyramiding value in the Properties tab accordingly.

- Close settings , Use dynamic TP and SL:

If enabled, script will exit all orders using the same but separate algorithm for moving averages. This enables the user to define if you want the orders to be closed if the price level of this moving average is hit. The price level for this calculation is visible on the chart by the blue line.

Although you can change the length and offset, as described underneath, this calculation uses the same data and source type defined in the Open settings area.

- Close settings , Length, Close:

This is the length used for the closing moving average calculations. 3 means it takes the last 3 bars of historical data for the calculation.

- Close settings , Offset, Close:

This defines if the calculation for the closing moving average should use an offset for the historical data. Just as the offset used for opening order, this does not use a look-forward feature, but a look-backward feature. To prevent any possible repaints the offset can only be positive, not negative.

For instance, if the length is 3 and the offset is 0 the calculation is made from the last 3 bars, making it bar1, bar2 and bar3. If the length is 3 and the offset is 1 the calculation is made from bar2, bar3, and bar4 – offsetting the calculation by 1 bar.

- Close settings , Use TakeProfit:

This toggle enables/disables a fixed take profit percentage.

- Close settings , TP %:

This sets the wanted % to reach on a take profit. This setting is ignored if the toggle above is disabled.

- Close settings , Use StopLoss:

This toggle enables/disables a fixed stop loss percentage.

- Close settings , SL %:

This sets the wanted % to reach on a stop loss. This setting is ignored if the toggle above is disabled.

Exit on Same Bar as Entry

By default, the script doesn't emit any exit orders on the same bar as the first entry order. Enable "Recalculation: After order is filled" to change this behavior.

Troubleshooting

While Pullback_Power is designed to provide reliable trading signals, you may encounter rare issues. One such issue could be receiving an error message stating "can't open orders with 0 or negative qty." If you encounter this error, it is likely due to specific conditions on the selected timeframe. To resolve this issue, change the timeframe on your trading chart.

Underlying Principles and Value Proposition

Pullback_Power leverages moving averages and volatility behavior to identify market retracements and capitalize on them. The strategy is rooted in the understanding that markets often experience temporary reversals or "pullbacks" before resuming their primary trend. By identifying these pullbacks and entering trades at opportune moments, Pullback_Power aims to capture quick profits from short-term market movements.

The dynamic and fixed calculations of Take Profit (TP) and Stop Loss (SL) levels enhances risk management, ensuring that potential losses are controlled while allowing room for profits to grow. The adaptive approach using the moving averages considers current market conditions, making the strategy flexible and responsive to changing volatility.

Moreover, Pullback_Power's non-repainting nature ensures the reliability of its signals, eliminating hindsight bias and providing traders with actionable insights based on real-time market data.

The strategy's simplicity and effectiveness make it accessible for traders of all experience levels. Whether you're a beginner looking to start scalping or an experienced trader seeking to diversify your trading approach, Pullback_Power offers a balanced blend of simplicity and sophistication to help you navigate the markets with confidence.

By focusing on clear, transparent principles and offering practical tools for risk management, Pullback_Power aims to provide tangible value to traders, empowering them to make informed decisions and optimize their trading outcomes.

Thank you for choosing Pullback_Power. I wish you successful trading!

Kioseff Trading - AI-Optimized RSIAI-Optimized RSI

Introducing AI-Optimized RSI: a streamlined solution for traders of any skill level seeking to rapidly test and optimize RSI. Capable of analyzing thousands of strategies, this tool cuts through the complexity to identify the most profitable, reliable, or efficient approaches.

Paired with TradingView's native backtesting capabilities, the AI-Optimized RSI learns from historical performance data. Set up is easy for all skill levels, and it makes fine-tuning trading alerts and RSI straightforward.

Features

Purpose : Uncover optimal RSI settings and entry levels with precision. Say goodbye to random guesses and arbitrary indicator use—this tool provides clear direction based on data.

Target Performance : You set the goal, and AI-RSI seeks it out, whether it's maximizing profits, efficient trading, or achieving the highest win rate.

AI-Powered : With intelligent AI recommendations, the tool dynamically fine-tunes your RSI approach, steering you towards ideal strategy performance.

Rapid Testing : Evaluate thousands of RSI strategies.

Dual Direction : Perfect both long and short RSI strategies with equal finesse.

Deep Insights : Access detailed metrics including profit factor, PnL, win rate, trade counts, and more, all within a comprehensive strategy script.

Instant Alerts : Set alerts and trade.

Full Customization : Test and optimize all RSI settings, including cross levels, profit targets and stop losses.

Simulated Execution : Explore the impact of limit orders and other trade types through simulation.

Integrative Capability : Combine your own custom indicators or others from the TradingView community for a personalized optimization experience.

Flexible Timeframes : Set your optimization and backtesting to any date range.

Key Settings

The image above shows explanations for a list of key settings for the optimizer.

Direction : This setting controls trade direction: Long or Short.

Entry Condition : Define RSI entry: Select whether to trigger trades on RSI crossunders or crossovers.

RSI Lengths Range : Choose the range of RSI periods to test and find the best one.The AI will find the best RSI period for you.

RSI Cross Range : Set the range for RSI levels where crosses trigger trade signals. The AI will find the best level for you.

Combinations : Select how many RSI strategies to compare.

Optimization Type : Choose the goal for optimization and the AI: profit, win rate, or efficiency.

Profit Target : Set your profit target with this setting.

Stop Loss : Decide your maximum allowable loss (stop loss) per trade.

Limit Order : Specify whether to include limit orders in the strategy.

Stop Type : Choose your stop strategy: a fixed stop loss or a trailing stop.

How to: Find the best RSI for trading

It's important to remember that merely having the AI-Optimized RSI on your chart doesn't automatically provide you with the best strategy. You need to follow the AI's guidance through an iterative process to discover the optimal RSI settings and strategy.

1.Starting Your Strategy Setup

Begin by deciding your goals for each trade: your profit target and stop loss. You'll also choose how to manage your stops – whether they stay put (fixed) or move with the price (trailing), and whether you want to exit trades at a specific price (limit orders). Keep the initial settings for RSI lengths and cross ranges at their default to give the tool a broad testing field. The AI's guidance will refine these settings to pinpoint the most effective ones through a process of comprehensive testing.

The image above shows our chart prior to any optimization efforts.

Note: the settings shown above in the key settings section will be used to start our demonstration.

2. Follow AI’s suggestions

Optimization Prompt: After loading your strategy, the indicator will prompt you to change the RSI length range and RSI level range to a better performing range.

Continue changing the RSI length range and RSI level range to match the indicator's suggestions until "Best Found" is displayed!

The image above shows results after we applied the tool’s suggestions. New suggestions have appeared, and we will continue to apply them.

Continue to adjust settings as recommended by the optimizer. If no better options are found, the optimizer will suggest increasing the number of combinations. Repeat this process until the optimizer indicates that the optimal setting has been identified.

Success! With the "Best Found" notification, an optimized RSI is now active. The AI will keep refining the strategy based on ongoing performance, ensuring continuous optimization.

AI Mode

AI Mode incorporates Heuristic-Based Adaptive Learning to fine-tune trading strategies in a continuous manner. This feature consists of two main components:

Heuristic-Based Decision Making: The algorithm evaluates multiple RSI-based trading strategies using specific metrics such as Profit and Loss (PNL), Win Rate, and Most Efficient Profit. These metrics act as heuristics to assist the algorithm in identifying suitable strategies for trade execution.

Online Learning: The algorithm updates the performance evaluations of each strategy based on incoming market data. This enables the system to adapt to current market conditions.

Incorporating both heuristic-based decision-making and online learning, this feature aims to provide a framework for trading strategy optimization.

Settings

AI Mode Aggressiveness:

Description: The "AI Mode Aggressiveness" setting allows you to fine-tune the AI's trading behavior. This setting ranges from “Low” to “High”, with “High” indicating a more assertive trading approach.

Functionality: This feature filters trading strategies based on a proprietary evaluation method. A higher setting narrows down the strategies that the AI will consider, leaning towards more aggressive trading. Conversely, a lower setting allows for a more conservative approach by broadening the pool of potential strategies.

Adaptive Learning Aggressiveness:

Description: When Adaptive Learning is enabled, the "Adaptive Learning Aggressiveness" setting controls how dynamically the AI adapts to market conditions using selected performance metrics.

Functionality: This setting impacts the AI's responsiveness to shifts in strategy performance. By adjusting this setting, you can control how quickly the AI moves away from strategies that may have been historically successful but are currently underperforming, towards strategies that are showing current promise.

Optimization

Trading system optimization is immensely advantageous when executed with prudence.

Technical-oriented, mechanical trading systems work when a valid correlation is methodical to the extent that an objective, precisely-defined ruleset can consistently exploit it. If no such correlation exists, or a technical-oriented system is erroneously designed to exploit an illusory correlation (absent predictive utility), the trading system will fail.

Evaluate results practically and test parameters rigorously after discovery. Simply mining the best-performing parameters and immediately trading them is unlikely a winning strategy. Put as much effort into testing strong-performing parameters and building an accompanying system as you would any other trading strategy. Automated optimization involves curve fitting - it's the responsibility of the trader to validate a replicable sequence or correlation and the trading system that exploits it.

Script a pagamento

Kioseff Trading - AI-Optimized Supertrend

AI-Optimized Supertrend

Introducing AI-Optimized Supertrend: a streamlined solution for traders of any skill level seeking to rapidly test and optimize Supertrend. Capable of analyzing thousands of strategies, this tool cuts through the complexity to identify the most profitable, reliable, or efficient approaches.

Paired with TradingView's native backtesting capabilities, the AI-Optimized Supertrend learns from historical performance data. Set up is easy for all skill levels, and it makes fine-tuning trading alerts and Supertrend straightforward.

Features

Rapid Supertrend Strategy Testing : Quickly evaluate thousands of Supertrend strategies to find the most effective ones.

AI-Assisted Optimization : Leverage AI recommendations to fine-tune strategies for superior results.

Multi-Objective Optimization : Prioritize Supertrend based on your preference for the highest win rate, maximum profit, or efficiency.

Comprehensive Analytics : The strategy script provides an array of statistics such as profit factor, PnL, win rate, trade counts, max drawdown, and an equity curve to gauge performance accurately.

Alerts Setup : Conveniently set up alerts to be notified about critical trade signals or changes in performance metrics.

Versatile Stop Strategies : Experiment with profit targets, trailing stops, and fixed stop losses.

Binary Supertrend Exploration : Test binary Supertrend strategies.

Limit Orders : Analyze the impact of limit orders on your trading strategy.

Integration with External Indicators : Enhance strategy refinement by incorporating custom or publicly available indicators from TradingView into the optimization process.

Key Settings

The image above shows explanations for a list of key settings for the optimizer.

Set the Factor Range Limits : The AI suggests optimal upper and lower limits for the Factor range, defining the sensitivity of the Supertrend to price fluctuations. A wider range tests a greater variety, while a narrower range focuses on fine-tuning.

Adjust the ATR Range : Use the AI's recommendations to establish the upper and lower bounds for the Average True Range (ATR), which influences the Supertrend's volatility threshold.

ATR Flip : This option lets you interchange the order of ATR and Factor values to quicky test different sequences, giving you the flexibility to explore various combinations and their impact on the Supertrend indicator's performance.

Strategies Evaluated : Adjust this setting to determine how many Supertrend strategies you want to assess and compare.

Enable AI Mode : Turn this feature on to allow the AI to determine and employ the optimal Supertrend strategy with the desired performance metric, such as the highest win rate or maximum profitability.

Target Metric : Adjust this to direct the AI towards optimizing for maximum profit, top win rates, or the most efficient profits.

AI Mode Aggressiveness : Set how assertively the AI pursues the chosen performance goal, such as highest profit or win rate.

Strategy Direction : Choose to focus the AI's testing and optimization on either long or short Supertrend strategies.

Stop Loss Type : Specify the stop loss approach for optimization—fixed value, a trailing stop, or Supertrend direction changes.

Limit Order : Decide if you want to execute trades using limit orders for setting your profit targets, stop losses, or apply them to both.

Profit Target : Define your desired profit level when using either a fixed stop loss or a trailing stop.

Stop Loss : Define your desired stop loss when using either a fixed stop loss or a trailing stop.

How to: Find the best Supertrend for trading

It's important to remember that merely having the AI-Optimized Supertrend on your chart doesn't automatically provide you with the best strategy. You need to follow the AI's guidance through an iterative process to discover the optimal Supertrend settings and strategy.

Optimizing Supertrend involves adjusting two key parameters: the Factor and the Average True Range (ATR). These parameters significantly influence the Supertrend indicator's sensitivity and responsiveness to price movements.

Factor : This parameter multiplies the ATR to determine the distance of the Supertrend line from the price. Higher values will create a wider band, potentially leading to fewer trade signals, while lower values create a narrower band, which may result in more signals but also more noise.

ATR (Average True Range) : ATR measures market volatility. By using the ATR, the Supertrend adapts to changing market volatility; a higher ATR value means a more volatile market, so the Supertrend adjusts accordingly.

During the optimization process, these parameters are systematically varied to determine the combination that yields the best performance based on predefined criteria such as profitability, win rate, or risk management efficiency. The optimization aims to find the optimal Factor and ATR settings.

1.Starting Your Strategy Setup

Begin by deciding your goals for each trade: your profit target and stop loss, or if all trades exit when Supertrend changes direction. You'll also choose how to manage your stops – whether they stay put (fixed) or move with the price (trailing), and whether you want to exit trades at a specific price (limit orders). Keep the initial settings for Supertrend Factor Range and Supertrend ATR Range at their default to give the tool a broad testing field. The AI's guidance will refine these settings to pinpoint the most effective ones through a process of comprehensive testing.

Demonstration Start: We'll begin with the settings outlined in the key settings section, using Supertrend's direction change to the downside as our exit signal for all trades.

2. Continue applying the AI’s suggestions

Keep updating your optimization settings based on the AI's recommendations. Proceed with this iterative optimization until the "Best Found" message is displayed, signaling that the most effective strategy has been identified.

While following the AI's suggestions, we've been prompted with a new suggestion: increase the

number of strategies evaluated. Keep following the AI's new suggestions to evaluate more strategies. Do this until the "Best Found" message shows up.

Success! We continued to follow the AI’s suggestions until “Best Found” was indicated!

AI Mode

AI Mode incorporates Heuristic-Based Adaptive Learning to fine-tune trading strategies in a continuous manner. This feature consists of two main components:

Heuristic-Based Decision Making: The algorithm evaluates multiple Supertrend-based trading strategies using metrics such as Profit and Loss (PNL), Win Rate, and Most Efficient Profit. These metrics act as heuristics to assist the algorithm in identifying suitable strategies for trade execution.

Online Learning: The algorithm updates the performance evaluations of each strategy based on incoming market data. This enables the system to adapt to current market conditions.

Incorporating both heuristic-based decision-making and online learning, this feature aims to provide a framework for trading strategy optimization.

AI Mode Settings

AI Mode Aggressiveness:

Description: The "AI Mode Aggressiveness" setting allows you to fine-tune the AI's trading behavior. This setting ranges from “Low” to “High”, with “High” indicating a more assertive trading approach.

Functionality: This feature filters trading strategies based on a proprietary evaluation method. A higher setting narrows down the strategies that the AI will consider, leaning towards more aggressive trading. Conversely, a lower setting allows for a more conservative approach by broadening the pool of potential strategies.

Optimization

Trading system optimization is immensely advantageous when executed with prudence.

Technical-oriented, mechanical trading systems work when a valid correlation is methodical to the extent that an objective, precisely-defined ruleset can consistently exploit it. If no such correlation exists, or a technical-oriented system is erroneously designed to exploit an illusory correlation (absent predictive utility), the trading system will fail.

Evaluate results practically and test parameters rigorously after discovery. Simply mining the best-performing parameters and immediately trading them is unlikely a winning strategy. Put as much effort into testing strong-performing parameters and building an accompanying system as you would any other trading strategy. Automated optimization involves curve fitting - it's the responsibility of the trader to validate a replicable sequence or correlation and the trading system that exploits it.

Script a pagamento

[Fedra Algotrading Strategy Trailing Stop Version]Simpler version of my popular strategy.Optimized for cryptocurrencies. Originally conceived to trade automatically through bots (that's how I use it), it also works to get signals and trade manually in any exchange.

It works in spot.

Buy the dip:

Attempts to buy on the dip, finding entries when the price makes abrupt dips that break deviation of the linear regression of the last periods.

Trend Detection:

Determines whether the market is in an uptrend or downtrend by crossing 2 SMAs + super trend in different temporalities. This affects the performance of the strategy. It works as a filter to avoid making entries in a downtrend.

% Trailing Stop Loss. The Stop Loss is placed a % below the price and accompanies it in the rises to make the most of an uptrend.

Optionally, you can set up a percentage Take Profit

It allows you to easily configure the backtest period to optimize the parameters for consistent results.

The strategy calculates by default a commission of 0.1% on each trade to make the backtest more "pessimistic".

Includes advanced features for compatibility with different bots platforms in the market.

Risk management by % of equity or by maximum series of losses.

////////////////////////////

Versión más simple de mi popular estrategia, optimizada para criptomonedas. Originalmente concebida para operar automáticamente a través de bots (así es como la uso yo), también funciona para obtener señales y operar manualmente en cualquier exchange.

Funciona en spot.

Compra en la caída:

Intenta comprar en la caída, encontrando entradas cuando el precio hace caídas abruptas que rompen la desviación de la regresión lineal de los últimos períodos.

Detección de tendencia:

Determina si el mercado está en tendencia alcista o bajista mediante el cruce de 2 SMAs + super trend en diferentes temporalidades. Esto afecta al rendimiento de la estrategia. Funciona como un filtro para evitar hacer entradas en contra de la tendencia del mercado.

% Trailing Stop Loss. El Stop Loss se coloca un % por debajo del precio y lo acompaña en las subidas para aprovechar una tendencia alcista.

Opcionalmente, se puede establecer un porcentaje de Take Profit

Permite configurar fácilmente el periodo de backtest para optimizar los parámetros y obtener resultados consistentes.

La estrategia calcula por defecto una comisión del 0,1% en cada operación para que el backtest sea más "pesimista".

Incluye características avanzadas para la compatibilidad con diferentes plataformas de bots en el mercado.

Gestión del riesgo por % del capital o por serie máxima de pérdidas.

BNBUSD 1 Minute Chart / 1 Hour BBand Day Trading 3Commas*** As always, this is provided for educational purposes only and I am not an investment advisor; I'm just a guy who likes to come up with novel ideas and share them with other traders so they can learn. ***

This strategy is a fun one. I took parts of 'Bollinger Awesome Alert R1 by JustUncleL' () and modified it to have enhanced day trading functionality. This version does not show source and that is by design - I want the alerts to be visible to the public and if you want to get set up with a version that integrates with 3commas, drop me a message - there's a lot more that goes into setting up automated 3commas trading but this script was written specifically with 3commas in mind.

It's possible this is one of the more interesting strategy indicators I've made. The setup I used for this is as such and you will need to set it up the same way:

One minute chart for the BNB/USD(T) pair on Binance.us (other exchanges will likely work, other coin pairs or other time frames will likely not)

This script watches the one minute chart and when price golden crosses the lower Bollinger band, a buy order is placed.

There are two sell conditions; one I set up to take profit and one I designed as a kind of stop loss. I went with a flat 7.5% for the take profit as this showed the best results in the backtester. I had planned for it to be closer to 3% but for this strategy to work it needs to be higher. According to the backtest it offers around double the return of buying and holding BNB over the sample timeframe.

The 'stop loss' condition is where the fun lies. I transposed Bollinger bands from a one hour BNBUSD Binance.us chart on top of the 1 minute chart and those are the blue lines you see. The stop loss condition happens when the current price death crosses the bottom one hour Bollinger band. Ironically, often this doesn't result in any losses as you will see in the chart and instead results in a small win. This definitely was not my intention when I created it but it's a lot better than the earlier version where I set up a variable percentage-based stop loss. Even with me optimizing the regular stop loss for this coin pair, my 1 hour bband method nets an extra 2% profit over the same two week time period, even with Binance fees factored in!

Have fun and like I said, hmu via message if you want access to the customizable indicator for 3commas!

Dankland Playground DCAing multi-strategy OPThis is essentially a script that I made for myself before deciding it may be good enough for you all as well.

How it works basically is this... you have 18 oscillators which can all be used as independently as you wish. That means there are 20 groups which they can be split amongst as you choose.

When in separate groups they should not be able to sell eachothers positions without triggering a stop loss. Every single oscillator has its own position sizing and exit sizing which can be stated as either a percent of balance or a flat amount of contracts. Each oscillator has a minimum amount of profit you can tell it to sell it, which is calculated from the average cost of your current position, which does include all groups. This works out to help you average out better entry and exit prices, essentially a method of DCAing.

You can set the minimum sale amount, which is to keep it from placing orders below your exchanges minimum dollar trade cost.

The included oscillators are as follows:

Chande Momentum cross

Moving Average Cross

MACD cross

%B Bollinger cross

Stochastic cross + region filter

Stochastic RSI cross + region filter

SMII cross and region

Three RMIs

Standard RSI

LSMA-smoothed RSI

Know Sure Thing

RSI of KST

Coppock Curve

RSI of Curve

PPO

RSI of PPO

Trix

RSI of Trix

So the idea is that this is essentially multiple strategies combined into one backtestable house. Balance is calculated for all position sizes in order to try to prevent false entries that plague so many scripts (IE, you set pyramiding to 2, each buy $1000, initial balance $1000, and yet it buys two orders off the bat for $2000 total and nets 400% profit because the second was considered free)/

You tune each side and position size them so that they work together as well as you can and in doing so you are able to create a single backtest that is capable of running a bot, essentially, between multiple strategies - you can run a slower Moving Average cross, a faster SMI cross or MACD, or Bollinger that grabs big moves only, all the while having MACD trade small bonuses along the way. This way you can weight the Risk to Reward of each against eachother.

I will not try to claim this is something you can open and with no work have the best bot on the planet. This scripts intention is to take a lot of relatively common trading strategies and combine them under on roof with some risk management and the ability to weigh each against eachother.